Every human being faces the same two-part dilemma in personal financial planning. First, we must figure out how to best utilize our skills and passions to earn a living. Second, we must decide how to best utilize that earned income to build a meaningful lifestyle.

Sure, some people earn a lot more money than others, which means they have more funds available to spend on needs, wants, and wishes. But at the end of the day, we must all decide what percentage of earned income to spend and save.

The percentage of income that you spend is called your personal spending rate, while the percentage of income that you save is called your personal saving rate. Both calculations are intimately (and inversely) related, and today I want to explore the relationship between saving, spending, and financial freedom.

Your Saving Rate and Financial Freedom

If you are new to this website, it might be helpful to read my introduction to financial freedom before proceeding. In the broadest context, financial freedom represents the same concept as “financial independence” and “retirement.” That is, the ability to spend your time however you see fit without regard to employment income.

You achieve financial freedom by building a passion business or investment portfolio that produces enough income to cover all living expenses. When your investments produce enough income to support your lifestyle, you no longer require a regular paycheck through standard employment, which means you’re financially free.

The only remaining question is how long it will take to reach that level of freedom. As detailed in the sections below, the amount of time that it takes to achieve financial freedom is primarily determined by your saving rate.

A Simple Thought Experiment

Let’s first explore the relationship between savings and freedom with the following thought experiment.

- If you save 5% of your income, you can take 1 year off for every 19 years worked.

- If you save 10% of your income, you can take 1 year off for every 9 years worked.

- If you save 20% of your income, you can take 1 year off for every 4 years worked.

- If you save 50% of your income, you can take 1 year off for every 1 year worked.

- If you save 80% of your income, you can take 4 years off for every 1 year worked.

- If you save 90% of your income, you can take 9 years off for every 1 year worked.

- If you save 95% of your income, you can take 19 years off for every 1 year worked.

Let’s assume $100,000 of income and apply this information.

- If you save $5,000 (5%) of your income, you are spending $95,000 (95%) annually

- You must work 19 years to accumulate enough savings to support 1 year of living expenses ($5,000 saved/year * 19 years = $95,000 required savings)

At the median values, things become more intuitive:

- If you save $50,000 (50%) of your income, you are spending $50,000 (50%) annually

- For every 1 year of work, you accumulate enough savings to support 1 year of freedom (BOGO every other year)

Now consider the other (highly unlikely) extreme:

- If you save $95,000 (95%) of your income, you are spending $5,000 (5%) annually

- After 1 year of work, you will accumulate enough savings to support 19 years of freedom ($95,000 / $5,000 = 19 years of freedom)

Although this thought experiment ignores the time value of money, I find it both motivational and insightful. The section below builds upon this information by adding other, more realistic economic assumptions to the equation. If you start to feel overwhelmed, return to the information presented in this section.

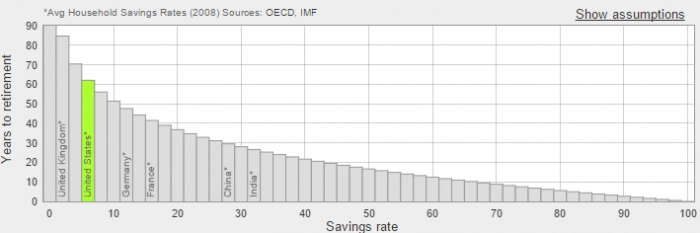

A Visual Explanation

We can input the information presented above into a free financial calculator called Networthify to visually illustrate the relationship between savings and financial freedom.

In my screenshot below (reinforced by the table presented in the next section), notice how this relationship is exponential in nature. Don’t mind the vertical axis titled “years to retirement.” Here, retirement is defined as the point when your investment income exceeds all expenses, making the term synonymous with financial freedom.

Networthify requires that we input the following information (my assumptions shown in parentheses below are pre-populated when you click the link, but feel free to modify given your situation):

- Annual after-tax income ($100,000)

- Current saving rate (varies according to your lifestyle)

- Current portfolio value ($0 – building wealth from scratch)

- 5% real annual return on investment (net of fees, taxes, and inflation)

- You will withdraw about 4% of the portfolio each year to spend

Once specified, Networthify does basic Excel calculations using these inputs. It’s nothing revolutionary, but I like the program because the interface is easy to use and understand.

Intuitively, the relationship between these inputs is straightforward. An increase in the saving rate, portfolio value, or ROI will reduce the amount of time required to reach financial freedom. What’s interesting to note is that annual income, by itself, doesn’t actually matter for these calculations. I explain why that is in the section below.

Using the Networthify assumptions detailed above, I’ve created a table that highlights the exponential relationship between saving rates and financial freedom.

| Saving Rate (Percent) | Years to Financial Freedom (Rounded) |

|---|---|

| 5 | 66 |

| 10 | 51 |

| 15 | 43 |

| 20 | 37 |

| 25 | 32 |

| 30 | 28 |

| 35 | 25 |

| 40 | 22 |

| 45 | 19 |

| 50 | 16.5 |

| 55 | 14.5 |

| 60 | 12.5 |

| 65 | 10.5 |

| 70 | 9 |

| 75 | 7 |

| 80 | 5.5 |

| 85 | 4 |

| 90 | 2.5 |

| 95 | 1.5 |

| 100 | 0 |

There are some interesting implications in this table. For example, if we apply these numbers to a recent college graduate:

- At a 10% saving rate, our college graduate must endure a 50-year working career before attaining freedom, which closely corresponds to traditional retirement age in America.

- At a 33% saving rate, that freedom timeline is cut in half (a little over 25 years).

- At a 50% saving rate, it will take about 16 years to find freedom, which means a college graduate who maintains a 50% saving rate should be able to “retire” before turning age 40.

- At a 66% saving rate, it will take roughly 10 years to find freedom.

- At an 80% saving rate, our college graduate finds freedom after five years of employment.

Each of these scenarios is a powerful reminder of the exponential relationship between savings and financial freedom. If you focus on increasing your saving rate, and nothing else, you will shave years off your personal financial freedom timeline.

How can that be?

The saving rate itself (not total income) is what determines the financial freedom schedule displayed in the table above. Recall from my saving rate tutorial, a saving rate is calculated as follows:

- (Income – Expenses) / Income = Saving Rate

You can increase your saving rate by increasing your income and/or decreasing your expenses. Surprisingly, a permanent decrease in spending will accelerate the financial freedom timeline more than an equivalent bump in income for two primary reasons:

1) As you spend less, you require less.

Recall from the intro, you achieve financial freedom when your investment portfolio produces enough passive income to cover all living expenses. Therefore, as you reduce your living expenses, you will automatically require a smaller investment portfolio to support your lifestyle.

2) As you spend less, you save more.

Holding income constant, a reduction in spending implies an increase in savings. As your saving rate increases, so too will the value of your investment portfolio. As your investment portfolio grows and compounds over time, it will produce more passive income each month, which will allow you to find freedom much sooner.

These statements should be reassuring, because although it can be difficult for some individuals to realize a significant bump in annual income, everyone can realize an immediate decrease in spending through careful lifestyle design.

What’s the takeaway?

The point of this article is not to say, if you save 50% of your income, you can stop working in exactly 16.6 years. Or, if you save 80%, you can “retire” in 5.6 years. Those are nonsensical predictions given the uncertainty of many economic assumptions made in Networthify.

For example, if the economy stagnates and your investment portfolio performs worse than expected, it might take a little longer to achieve financial freedom. That’s not a problem you should worry about because you cannot predict how future changes in the world economy will impact financial markets.

But the relationship between savings and financial freedom is concrete and something that you can control directly. Therefore, you should use the information presented in this article as motivation to modify your lifestyle and increase your saving rate.

With that said, the optimal saving rate will vary according to your personal preference for financial freedom.

If you enjoy your career and find your daily routine meaningful, you may have very little interest in saving the vast majority of your income each year. Perhaps you would rather spend freely on the goods, services, or activities that you find enjoyable. That’s perfectly fine as long as you recognize the inverse relationship between consumption and financial freedom.

If, however, you are unhappy in your current employment, make the conscious decision to prioritize and increase your saving rate through the following actions:

- Begin tracking your income and spending using a free Personal Capital account.

- Stop spending money on trinkets, gadgets, gifts, or services that you don’t need.

- Increase your earning potential by learning a new skill, starting a business, or applying for a new job.

In our journey to financial freedom, Vanessa and I modified every aspect of our lifestyle to realize an increase in savings. If you would like to know more, our Minimalist Living Guide is sure to spark your own creative efforts.